The case for a radical overhaul of the way that motoring is taxed is set out in a report, funded by the RAC Foundation, that we are publishing today. We recommend a move to a widespread system of road pricing. The revenues raised could be used to reduce other motoring taxes. Such a move would generate substantial economic efficiency gains from reduced congestion, reduce the tax levied on the majority of miles driven, leave many (particularly rural) motorists better off, and provide a stable long-term footing for motoring taxes without necessarily raising net additional revenue from drivers.

The economic rationale for road pricing is compelling. Road use generates costs which are borne by wider society instead of the motorist. These 'externalities' mean that in the absence of taxation or pricing, there is an inefficiently high level of road use. Taxes can help bring private demands into line with the socially desirable level. Several different externalities are associated with motoring. Some, like carbon emissions from burning petrol and diesel, are easily addressed through fuel duties as the costs depend entirely on fuel use. Others, notably congestion but also the costs of noise and accidents, vary enormously according to where and when someone drives. Driving in rural areas late at night imposes no congestion cost upon other motorists. Driving in conurbations at rush hour generates large congestion costs. Taxes on fuel cannot vary according to time and location, and so are fundamentally unable to account for this variation. Taxes on road use, however, would be able to do so. The potential efficiency gains from better-targeted taxes are large: the 2005 Eddington Review estimated benefits of up to £25 billion per year.

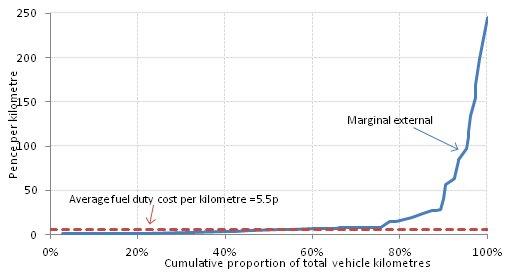

The figure below illustrates the point. Drawing on figures from the Department for Transport, it shows an estimate of the marginal external cost associated with each kilometre of road use from least costly on the left to most costly on the right. They vary enormously from just 0.9p per kilometre to 245p per kilometre (and, if anything, these figures probably understate the variation in the marginal externality). For a car of average efficiency, driving a kilometre leads to a fuel duty payment of around 5.5p irrespective of location and time. The bluntness of fuel duties is clear. Even ignoring other taxes on motoring, perhaps half of kilometres are taxed too much, one-quarter taxed at roughly the appropriate level, and one-quarter taxed too little, often substantially so.

Figure 1. The distribution of the marginal external costs of motoring

Source: Authors' calculations based on Department for Transport (DfT) data.

Notes: The marginal external cost distribution is derived using estimates of the total motoring externality for all major types of road (conurbation, urban and rural) across different congestion bands. These have been weighted to construct the distribution by using estimated 2010 values of the proportion of total distance driven on each combination of road type / congestion band.

There is a second, fiscal, argument for road pricing. Fuel duties and Vehicle Excise Duty (VED) raise around £38 billion per year. But these revenues do not appear to be sustainable in the medium-term. Forecasts from the Office for Budget Responsibility suggest that by 2029/30, revenues from these taxes will be some 0.9% of national income lower than today. This equates to more than £13 billion per year in current terms. This decline is partly down to improved vehicle efficiency and the growth of electric vehicles. In the extreme case in which all vehicles were electric, revenues from fuel taxes and VED would disappear altogether - but the problems of congestion would clearly remain.

How could this revenue be replaced? £13 billion is approximately equivalent to a 3½p increase in the basic rate of income tax, an increase in the main rate of VAT to almost 23%, or a 50% rise in rates of fuel duties. None of these options are particularly palatable, and there is little sense in ever higher fuel duty rates for the shrinking base of motorists relying on conventional fuel. Indeed, the difficulty of sustaining revenues through further duty rises has already been demonstrated by the consistency with which both this government and its predecessor have announced, and then failed to implement, duty increases. From their peak in March 1999, real (inflation adjusted) fuel duty rates were 16% lower by December 2010. Real fuel duty per kilometre driven fell by 13% between 2000 and 2010, from 6.3p to 5.5p.

Road use, however, appears to be a more sustainable tax base. The Committee on Climate Change estimates that total distance driven in the UK will rise by almost one-quarter from 516 billion vehicle kilometres in 2010 to 637 billion by 2030. Revenues from road pricing would not erode as vehicles become more efficient, and the charge - assuming it varied by where and when the driving occurred - would provide the right signals to deal better with variation in congestion costs.

As we have argued elsewhere, there are multiple long term pressures on taxes and spending. Just as we need prepare for, and debate how to pay for, demographic change, so we should be taking the time to debate and design a system of road pricing. The groundwork needs to be laid now. In this context the potential reforms to ownership of the strategic road network recently outlined by the Prime Minister simply enhance the need for a sensible, joined-up strategy. Before signing long-term leases to let private firms manage key roads, the government should consider carefully whether this would compromise the ability to implement national road pricing if it - or a future government - were finally to accept the overwhelming logic for it in the years ahead.

Authors

Andrew Leicester

Paul Johnson

Paul has been the Director of the IFS since 2011. He is also currently visiting professor in the Department of Economics at University College London.

George Stoye

I completed a PhD at UCL in 2020. My work examines the drivers of variation in the quantity and quality of healthcare provided to different patients.

More from IFS

Understand this issue

Policy analysis

Academic research