On Tuesday afternoon MPs will debate the recent report by the Work and Pensions Select Committee on “intergenerational fairness”. Drawing on evidence the IFS, the committee argued that triple lock indexation of the state pension should not continue beyond 2020.

For a given amount of spending on state pensions there is a trade-off between the level of the state pension and the state pension age from which it is paid. With the triple lock a full single-tier pension in 2060 is projected to be worth 27.5% of average earnings and will be available from age 69. If we were to abandon the triple lock and instead index in line with average earnings beyond 2020, then a full single-tier pension in 2060 would be projected to be worth 24.2% of average earnings. For the same cost as the triple lock this could be paid from roughly age 67½. Alternatively if we wanted a higher pension at, say, 30.7% of average earnings then keeping within the same cost envelope could be achieved by increasing the pension age further to roughly age 70½.

The triple lock states that each year the state pension will increase by the highest of the increase in earnings, the increase in prices (as measured by the Consumer Price Index) and 2½%. Over the longer term this would eventually prove to be a financially unsustainable method of indexation. This is because every time earnings grow by less than either 2½% or prices then the value of the state pension would ratchet up as a share of average earnings.

Of course it is not unreasonable to argue that the state pension should be made more generous (though it is should be remembered that – as IFS research has shown – pensioners are no longer a particularly poor group in society). But if the government wants to increase the level of the state pension relative to earnings, it should choose the level it wants (and potentially a path to get there) rather than allowing the somewhat haphazard increases relative to earnings that result from the triple lock. The last few years – in which earnings growth has been extremely weak – have seen triple lock indexation boost the value of the state pension dramatically, relative to both average earnings and prices. Between April 2010 and April 2016 the value of the state pension has been increased by 22.2%, compared to growth in earnings of 7.6% and growth in prices of 12.3% over the same period. This has pushed the value of the basic state pension up to its highest share of average earnings since April 1988. This increased benefit to pensioners came at the cost of an increase in spending of roughly £6 billion a year in 2015–16 compared with earnings indexation, and roughly £4 billion relative to CPI indexation, over the period since April 2011.

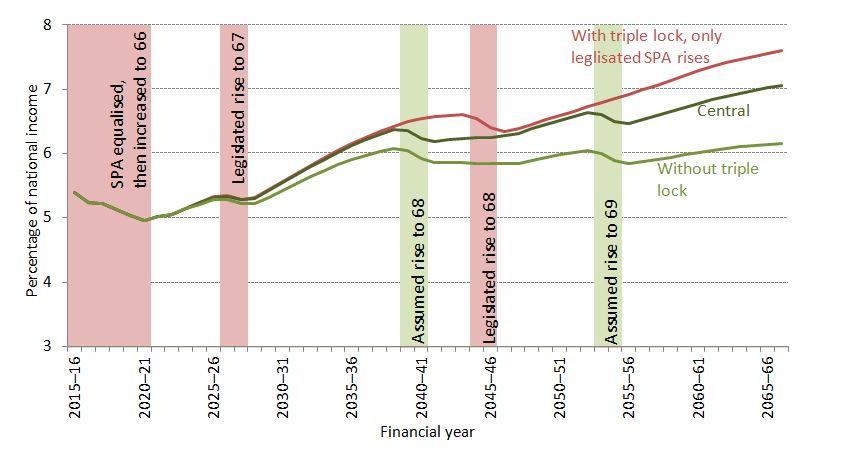

Projecting the cost of the triple lock (relative to linking the level of the state pension to earnings growth) over the longer-term is difficult. If the economy delivers strong growth in earnings, without periods of boom and bust, then the lock would seldom apply and the state pension would mostly grow in line with earnings. But if the economy delivers weak and/or volatile earnings growth then the value of the state pension would, over time, ratchet up relative to average earnings. In its January 2017 Financial Sustainability Report the OBR projected state pension spending over the next fifty years under both the triple lock and an alternative scenario of earnings-indexation beyond the end of this parliament, with the cost of the triple lock being based on movements in earnings and prices over the thirty years from 1991 to the end of the their current forecast period in 2021. These projections are shown in the Figure below. Without the triple lock – the series shown in light green at the bottom of the figure – spending is projected to increase by 1.1% of national income between 2020–21 and 2060–61 (from 5.0% to 6.0%). This is equivalent to £21 billion in today’s terms. Under the triple lock spending (as shown by the dark green line) is projected to rise by 1.8% of national income over the same period (from 5.0% to 6.8%), which is equivalent to £35 billion in today’s terms, or some £15 billion more than under earnings indexation.

Figure. OBR projections of state pension spending

Source: Table 3.2, page 35 and Chart 3.10, page 58, of Office for Budget Responsibility, Financial Sustainability Report, January 2017, (http://cdn.budgetresponsibility.org.uk/FSR_Jan17.pdf).

Both these projections assume that the Government raises the state pension over time in line with the intention, announced by the then Chancellor George Osborne in the 2013 Autumn Statement, “that people should expect to spend, on average, up to one third of their adult life in receipt of the State Pension”. Recommendations on the level of the state pension age beyond 2028 (by when it is due to have reached age 67) are to come in the next couple of months from the independent review led by John Cridland. But on the basis of the “one third of adult life” statement from the Government, and the latest central longevity forecasts from the Office for National Statistics, the OBR calculates this would see the state pension age for men and women rise to 68 by 2041 and to 69 by 2055. This is in contrast to current legislation which has it rising to age 68 by 2046 and then not rising any further.

The OBR also projects state pension spending under the scenario where the triple lock is left in place, but that the state pension age rises only in line with the already legislated increases. This is shown in the red line at the top of this figure. Under this scenario projected spending in 2060–61 is 0.5% of national income – or £10 billion in today’s terms – higher than under the central scenario.

This implies that a one year increase in the state pension age (from age 68 to 69) by the mid 2050s reduces projected state pension spending in 2060–61 by 0.5% of national income, or £10 billion in today’s terms. But in the same year the triple lock is projected to cost 0.8% of national income, or £15 billion, more than under earnings indexation alone. Therefore these projections imply that, over the next forty years, the additional cost of triple lock – rather than earnings – indexation is roughly equivalent to the cost of increasing the state pension age by 1½ fewer years. So, in other words, keeping the triple-lock and increasing the state pension age to 69 in the mid-2050s might have similar public finance implications to moving to earnings indexation and instead only increasing the state pension age to 67½.

That is not to say that if we were to abandon the triple lock then the state pension age should increase less quickly. After all, as the Figure above shows, earnings-indexation of the state pension along with increases in the state pension age to 69 by the mid 2050s still leads to projected spending increasing as a share of national income over the next fifty years. If instead we scrapped the triple lock the scale of the increase in spending on the state pension – and therefore the cuts to spending elsewhere, or tax rises, needed to fund it – would be substantially reduced.

Authors

Carl Emmerson

Carl, a Deputy Director, is an editor of the IFS Green Budget, is expert on the UK pension system and sits on the Social Security Advisory Committee.

More from IFS

Understand this issue

Policy analysis

Academic research