Downloads

Download working paper here

PDF | 603.85 KB

Like most other developed countries, income and productivity growth has been very slow in the UK since the financial crisis of 2008–09. But on a per person basis, economic growth has been slower than in the US, the EU27 and Germany in that time. The slowdown has been particularly stark given that the UK economy, and its productivity, were growing quite quickly prior to 2008. While employment growth has been strong, average earnings growth has been dreadful - for which read almost non-existent. Gross Domestic Product per head is today nearly £11,000 lower than it would have been had pre crisis trends continued.

Much of that slowdown is a result of international factors well outside the control of any government: the fallout from the financial crisis, Covid, the energy price spike. But low investment, policy mistakes, political instability, and Brexit, have combined to hold back growth by more than in many comparable nations.

In a contribution to Anthony Seldon and Tom Egerton’s forthcoming book The Conservative Effect, 2010-2024, we document the course of the economy over the last 14 years.

1. Introduction

From the moment the Coalition government was formed following the general election in May 2010, the new prime minister, David Cameron, stated that its first priority was to ‘reduce the deficit and restore economic growth’1 .

The parliament from 2010 to 2015 was certainly dominated by the fiscal consolidation, more widely known as austerity. The Global Financial Crisis (GFC) had opened up a budget deficit – that is the difference between total government spending and total government revenues – that was at a record high for the UK since 1946–7 and the focus on getting it down involved cuts to public spending on a scale that had not been delivered in recent decades. Despite the shock of the Brexit referendum result, by 2019, the current budget – that is the gap between total government revenues and non-investment spending – had, just about, been returned to surplus.

The twin shocks of Covid-19 and the subsequent ‘cost of living crisis’ saw the deficit grow again, reaching a new record high in 2020–1. As we approach another general election the fiscal situation continues to dominate economic debate as the combined effects of these three shocks on borrowing has been to leave government debt at above 90 per cent of national income, more than twice its pre-financial crisis level (of around 35 per cent), and not falling. In contrast to the period between 2010 and 2019, the parliament that began in December 2019 has seen big increases in both spending and tax.

While the deficit did fall from 2010 to 2018 it was more painful and more protracted than originally planned. It was blown off course by events. The record on restoring growth has been even worse. The UK’s economy grew slowly throughout the 2010s, and has struggled to weather the shocks of the 2020s. Productivity and national income per capita have been virtually stagnant, with serious implications for wages and living standards.

These two key themes of the last fourteen years have intertwined. Poor growth has driven the increase in the size of the national debt relative to national income.

The 2010s were remarkable not only for poor economic performance and the scale of public spending retrenchment, but also for the loosest monetary policy in history. The Bank of England Bank Rate never rose above 0.75 per cent between March 2009 and May 2022. It had never been that low before in the more than 300-year history of the Bank of England. That pushed up asset prices, including house prices, and combined with tight fiscal policy and terrible earnings growth to entrench an advantage for an older, wealthier generation. Higher inflation and sharply increased interest rates present new challenges at the tail end of this period.

We start this chapter with an overview of the performance of the economy since 2010, where we discuss growth, productivity and wages. We then discuss the possible causes of the poor performance, and what policymakers did, or didn’t do, that might have contributed to it. Next, we turn to an overview of the two distinct eras of fiscal policy since 2010: the austerity and then policy stagnation of 2010 to 2019, followed by fiscal responses to the series of shocks the UK weathered from 2019 to 2024. Finally, we touch on the monetary policy of the Bank of England, and how it interacted with government policy throughout the period.

2. The State of the Economy

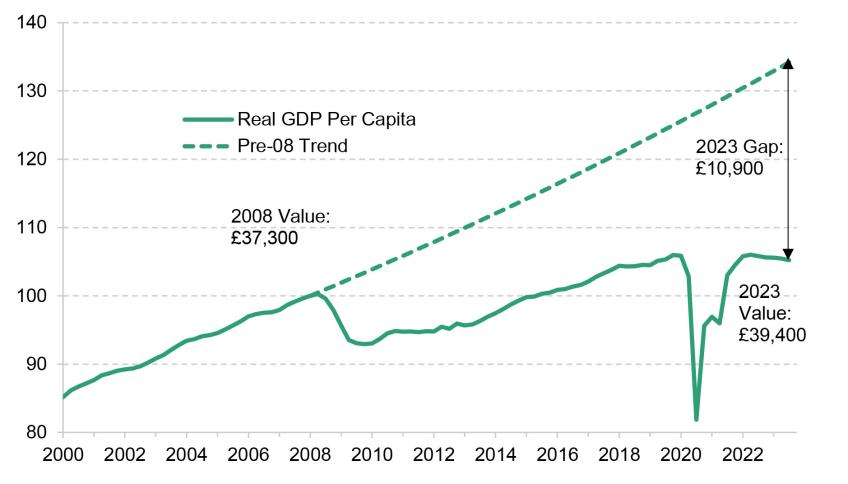

Relative to the decades leading up to the Global Financial Crisis, the performance of the economy has been very poor. Figure 2.1 highlights this. The solid line shows actual GDP per capita, the dashed line what it would have been had growth continued on its pre-financial crisis path. If this had happened, GDP would have reached £50,200 per person, a 35 per cent increase since 2008. Instead, it was £39,400, an increase of just 6 per cent over a fifteen-year period. Economic growth this slow over this long a period has no precedent in the UK since at least the end of World War II.

Figure 2.1 GDP per capita compared to pre-recession trend

Note: Indexed, 2008 values equal to 100. Pre-recession trends based on authors’ calculations of growth rate from 2000 to 2008.

Source: Office for National Statistics series IHXW (Gross domestic product (Average) per head, CVM market prices: SA).

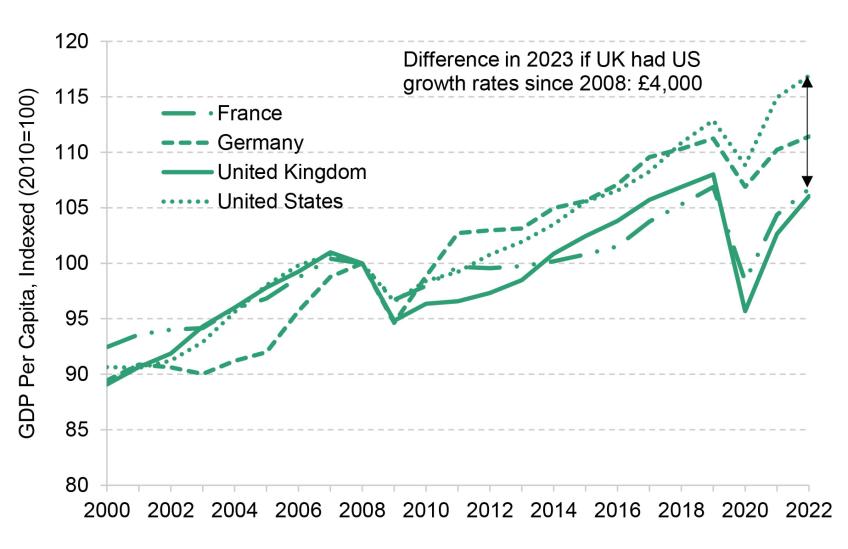

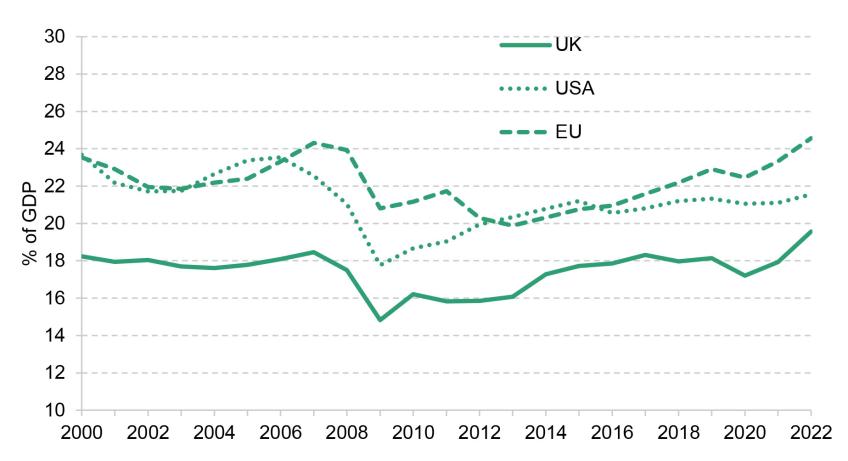

The international comparison in Figure 2.2 demonstrates that the UK is not unique. Other major European economies like Germany (which had done much better through the Global Financial Crisis) and France have also experienced historically slow growth over this period. The United States has done somewhat better, especially since 2019, reflecting in part both different effects of economic shocks and quite different policy responses. While differences are not huge over the period as a whole, the UK has performed poorly since 2019, relative both to past performance and to some other countries. This has taken the form both of a bigger hit to the economy than other countries during the Covid-19 pandemic, and a relatively sluggish recovery from it.

The EU27 as a whole has done rather better. GDP per capita grew by 14 per cent between 2008 and 2023, in part reflecting catch-up by some of the former communist countries like Slovenia and the Czech Republic, which now have similar levels of GDP per capita to the UK when measured on a Purchasing Power Parity basis.

Figure 2.2 GDP per capita compared to France, Germany and the US

Note: Difference comparisons based on authors’ calculations. Differences expressed in 2023 prices.

Source: IMF World Economic Outlook Database.

For much of the period what became known as the ‘productivity puzzle’ lay at the forefront of the debate about poor growth in the UK and across Europe2 . Figure 2.3 shows how the economy has continued to struggle with low productivity growth. There was strong growth in labour productivity in the run-up to the Global Financial Crisis. Since then labour productivity has almost entirely stalled: it is only 7 per cent higher than it was in 2008. The UK’s labour productivity has lagged behind other countries much more than its GDP and GDP per capita have: output per hour worked has since 2008 grown more slowly in the UK than in every G7 country besides Italy. Big increases in the employment rate have boosted UK output, but it will not be possible for the employment rate to grow forever. For GDP per capita to continue to keep pace with even the poor economic performance seen in Western European, let alone return to pre-Great Recession growth rates, productivity will need to improve.

Figure 2.3 Labour Productivity Compared to Pre-Recession Trend

Note: Indexed, 2008 values equal to 100. Pre-recession trends based on authors’ calculations of growth rate from 2000 to 2008.

Source: Office for National Statistics series LZVB (UK Whole Economy: Output per hour worked SA).

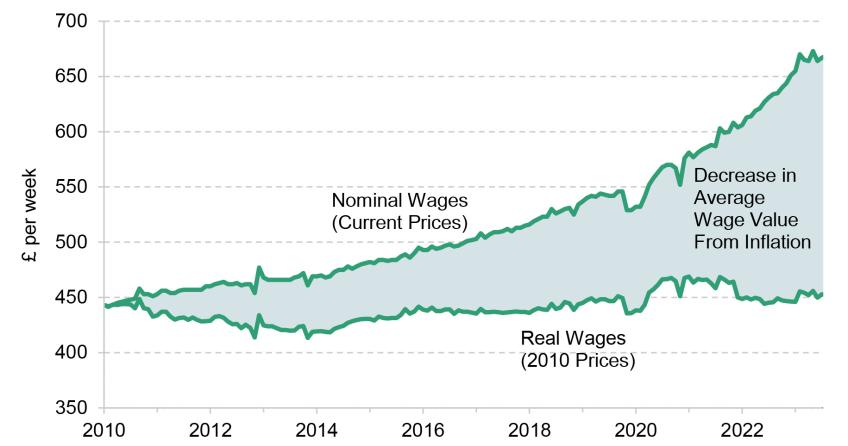

The minimal productivity growth since 2010 has also had meaningful negative consequences for living standards. Poor growth in output per hour worked has passed through to a stagnation in the wages workers receive. Figure 2.4 shows how nominal and real wages have changed since the Conservatives took office. The top line shows that in nominal terms, the average earnings of UK employees have increased from £450 to £650 per week. However, when accounting for inflation, there has been no increase in real wages in that time: £650 was worth as much in 2023 as £450 was in 20103 . Unusually for the aftermath of economic downturns, there was no recovery in real wages following the Great Recession, with real wages continuing to drop until 2014, since which they have very slowly recovered to 2010 levels. This lack of growth in real wages is unprecedented in the last two hundred years of British economic history: there has been no longer period without growth in real wages since the Napoleonic Wars4 .

Figure 2.4 Nominal and real wages since 2010

Note: Measured in Average Weekly Earnings, £

Source: Office for National Statistics Series KAB9 (AWE: Whole Economy Level (£): Seasonally Adjusted Total Pay Excluding Arrears) and Series D7BT (CPI INDEX 00: ALL ITEMS 2015=100)

This has, naturally, created a significant drag on working-age household incomes, which have also grown much more slowly than before the Great Recession. Without wage increases, only increased levels of employment have pushed up incomes among working-age households. (Benefits and tax credits have been cut, and taxes overall have risen.) Meanwhile, household incomes for those over 65 have increased, as a result of increased income from pensions, leading to a dramatic increase in the proportion of pensioners at the top 15 per cent of the income distribution, and a decrease in the proportion in the bottom 15 per cent of the income distribution, while the trend for working-age households has gone the other way, held back by lagging wages5 .

Meanwhile, there has been little change in income inequality, at least across the bulk of the distribution. Wages at the bottom of the distribution have been boosted by significant increases in the living wage/minimum wage and earnings by increased levels of employment, but this has been offset by cuts to benefits and tax credits. At the top end, at least as far as the 95th percentile, wages have been stagnant and, for some of the highest earners, taxes have risen quite sharply6 .

3. The Productivity Puzzle Revisited

The UK’s struggling productivity can be broken down into two periods. The first is the period until 2019, under the premierships of David Cameron and Theresa May, where growth was poor, but not uniquely so compared to other advanced economies. The second is that covered by the parliament of 2019 to 2024, under the premierships of Boris Johnson, Liz Truss and Rishi Sunak, where the UK emerged from a turbulent time for the global economy having fallen behind its neighbours.

One of the problems in determining the cause of the productivity slowdown is that many of the candidate explanations have been much longer standing than the slowdown itself. For example, investment (public and private) as a share of GDP fell sharply after the Great Recession, and has remained below the rest of the G7. However, as Figure 3.1 shows, the UK had a relatively low level of investment since long before the Conservatives came to office. Some of this can most likely be put down to the heavier focus of the UK economy on services, which are less capital intensive, but it is hard not to suspect that the UK may be suffering from chronic underinvestment, with little progress since 2010.

Public investment levels fell sharply in 2010 as capital spending was cut as part of the response to the record deficit. Low public investment over most of the 2010s is perhaps particularly noteworthy given the historically low interest rates at which the government could borrow during the period. Indeed, then permanent secretary to the Treasury Nick, now Lord, Macpherson said in 2023 ‘With hindsight we probably should have taken advantage [of low interest rates] and borrowed more when times were more stable … and invested more.7 ’ Capital spending was ramped up later in the period, reaching its highest level in decades by the early 2020s. But by 2023 the forward plans were to cut the real level of capital spending over the subsequent five years. Here, as elsewhere, the lack of consistency in economic policy over the period from 2010 to 2023 has been quite striking – sharp cuts, followed by an increasingly serious increase, followed by further planned cuts.

The inconsistency of public investment is perhaps best exemplified by High Speed 2, aimed at increasing rail speed and capacity between London, Birmingham, Manchester and Leeds. Announced by the then chancellor George Osborne, it was subject to frequent discussions about whether it should be cancelled by successive chancellors long after construction had already begun, before the Leeds connection was dropped by Boris Johnson and the Manchester connection dropped by Rishi Sunak. This inconsistency only serves to add risk for firms looking to make long-term investment decisions.

Figure 3.1 Investment levels compared to the US and EU

Note: Gross Fixed Capital Formation as a % of GDP

Source: IMF World Economic Outlook Database

The path of the corporation tax rate has demonstrated this lack of consistency even more powerfully. Between 2010 and 2018 George Osborne and then Philip Hammond gradually brought down the main rate from 28 to 19 per cent, in an effort to spur private sector investment. By 2023 the headline rate had returned to 25 per cent though even that reversal was not without its own convoluted path – the new higher rate having been announced by Mr Sunak while he was chancellor, reversed during the 38-day chancellorship of Kwasi Kwarteng and then reinstated by Jeremy Hunt on the day he replaced Mr Kwarteng. Aside from the merits of lower corporation tax for encouraging investment, the uncertainty created around policies intended to encourage businesses to invest in the UK has most likely served only to discourage such investment.

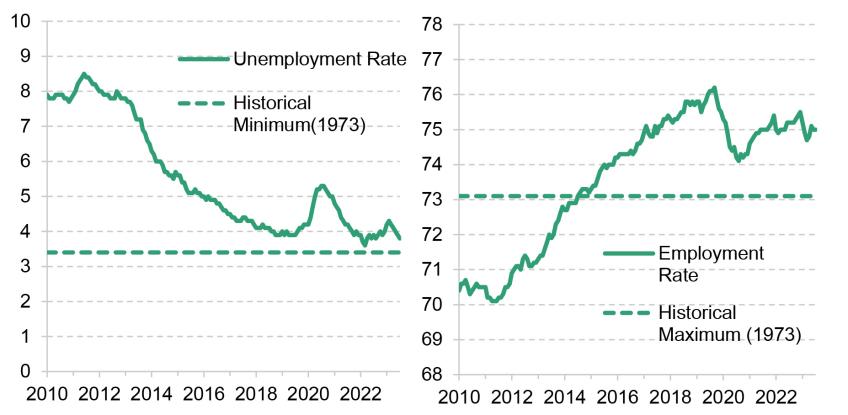

One major macroeconomic success may provide another part of the answer to the productivity puzzle: employment has boomed, and unemployment has remained remarkably low. The left chart on Figure 3.2 shows the course of the unemployment rate over the Conservatives’ time in power. While it was high after the Great Recession, it fell to near historic lows over the premierships of Mr Cameron and Mrs May, and has stayed there in spite of stormy global macroeconomic conditions. This cannot simply be explained by workers leaving the labour force, either: the right chart on Figure 3.2 shows that the employment rate has gone far past historic highs, as more and more people have entered the labour force with particularly strong growth in the employment rate among women. The paradigm shift to low unemployment and high employment has been a welcome development, and has helped keep household income rising in spite of stagnant wages, and has helped to boost GDP per capita. However, it may have also contributed to lower productivity: at lower levels of unemployment, less productive workers have entered the labour force. This is clearly not the main explanation for poor productivity, but to the extent that it plays a role, it is less of a problem.

Figure 3.2. Unemployment and employment rates since 2010

Note: All figures shown as a percentage. Historical Data From Records Since 1970.

Source for Unemployment Rate: Office for National Statistics Series MGSX (Unemployment rate, aged 16 to 64, seasonally adjusted). Source for Employment Rate: Office for National Statistics Series LF24 (Employment rate, aged 16 to 64, seasonally adjusted).

The capacity of the economy to produce jobs is understated even by these figures. Rising activity rates, increases in the state pension age, and substantial net immigration have between them led to an increase of around 4 million in the number of people in employment between 2010 and 2023 – an increase from 29 million to 33 million8 .

The 2016 referendum vote to leave the European Union and eventual exit in January 2020 has also had harmful impacts, though their precise scale is hard to disentangle from the impacts of Covid-19. Several academic analyses have attempted to estimate how UK exports have been affected. The decision for the UK – apart from Northern Ireland – to leave the single market led to new non-tariff barriers to trade for British exporters. The evidence suggests that this significantly damaged exports of goods, particularly where firms form part of global manufacturing supply chains9 .

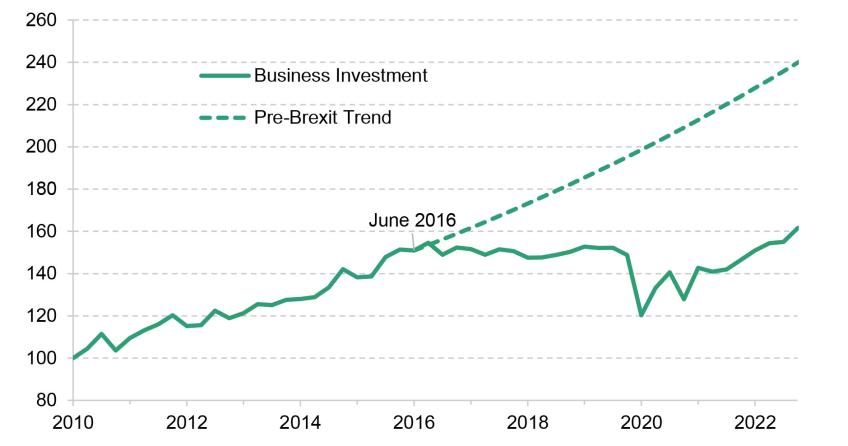

Figure 3.3 shows business investment since 2010. There is a sharp fall relative to the post-2010 trend from around the date of the June 2016 referendum: the uncertainty created by the Brexit vote, and associated political turmoil, appears to have led to a substantial decrease in business investment relative to what we might otherwise have expected. Indeed, by the start of 2023 business investment in the UK was no higher than it was in June 2016 – a phenomenon not replicated in other advanced economies. This gap between the pre-Brexit trend and the outturn amounts to approximately £4,200 per worker per year by 2023 and a shortfall of this magnitude can be expected to have negative consequences for growth. Frequent shifts in possibility of different outcomes of the Brexit negotiations, from an anticipation of remaining in the single market in pre-referendum rhetoric to frequent high-profile threats of a ‘No Deal’ Brexit with tariffs on trade, most likely damaged investment in Britain more than a less chaotic strategy that led to the same post-Brexit arrangements with the EU would have done.

Figure 3.3 Business investment compared to pre-Brexit trend

Note: Indexed, 2010=100. Deflated according to GFCF Deflator. Pre-Brexit vote trend based on authors’ calculations.

Source: Office for National Statistics, Series NPEL (Gross Fixed Capital Formation: Business Investment: CVM SA).

One expected consequence of Brexit that has not materialised is a sharp decline in overall immigration. A decline in immigration from the EU has occurred, but it has been more than made up for by an increase in immigration from outside the EU, though the skill mix and location of workers has been affected by this shift.

In total, quantitative estimates based on comparisons to similar countries estimate the negative effect of Brexit on economic activity to be equivalent to approximately 5 per cent of GDP10 . The Office for Budget Responsibility (OBR) judges that post-Brexit trading arrangements will reduce UK productivity by 4 per cent relative to remaining in the EU11 . However, it is worth noting that it is incredibly hard – to say the least – to disentangle the impact of Brexit from other growth issues the UK has faced since 2016, particularly those that did not affect comparable countries12 . In the years since 2019, the global economy was hit by shock after shock, which the UK will have different exposures to and may have dealt with comparatively worse.

The first of these is the Covid-19 pandemic. In all countries, this created a major downturn in output, as economic activity stalled – first because of precautions even in sectors such as manufacturing and construction and then for a much longer time after that in public-facing sectors, with demand completely eliminated in many service sectors. At the time of writing it appears that the UK economy has recovered less well than many others from the effects of Covid – though it is worth saying that problems with measurement and the interpretation of economic data through this period make even this judgement subject to some uncertainty.

The UK’s response to the pandemic was, fiscally, bigger than that in most other countries. The Coronavirus Job Retention Scheme (CJRS) announced by the then chancellor Rishi Sunak, widely known as furlough, subsidised the wages of many private-sector employees who did not work during the pandemic, in an attempt to preserve the links between employees and employers. Many European governments implemented similar policies, in an attempt to ensure that employees could return to their jobs quickly. However, the United States took a different approach, and rebounded much quicker from the pandemic. Instead of preserving worker-firm links, they implemented generous unemployment insurance, which meant that workers searched for new jobs as the economy reopened. Given that the post-pandemic economy looked rather different from the pre-pandemic economy, this freedom to seek out other work may well have helped productivity in the US. In contrast, the Conservatives maintained the furlough scheme, which kept employees attached to their pre-Covid jobs, until the autumn of 2021, when all restrictions on movement and gatherings had been lifted. The gross cost of the CJRS scheme over the nineteen months it was in place came to £70 billion, with a further £28 billion spent on support for the self-employed. The untargeted scheme looks to have been maintained for too long, slowing the reallocation of workers to new sectors. It may well have harmed productivity in the aftermath of the pandemic, as workers remained at jobs that did not realise their full potential.

As the significance of Covid-19 waned, another major shock hit Western economies. The Russian invasion of Ukraine caused a major upwards shock to global oil and gas prices. This created fewer problems for countries with greater energy independence, either because they had their own sources of fossil fuels, like the US, or because they mostly used nuclear power, like France. Since the UK’s energy supply mostly comes from gas, the UK economy may well have suffered more, with inflation persisting for longer potentially necessitating greater and more damaging action to bring it down.

4. The Public Finances

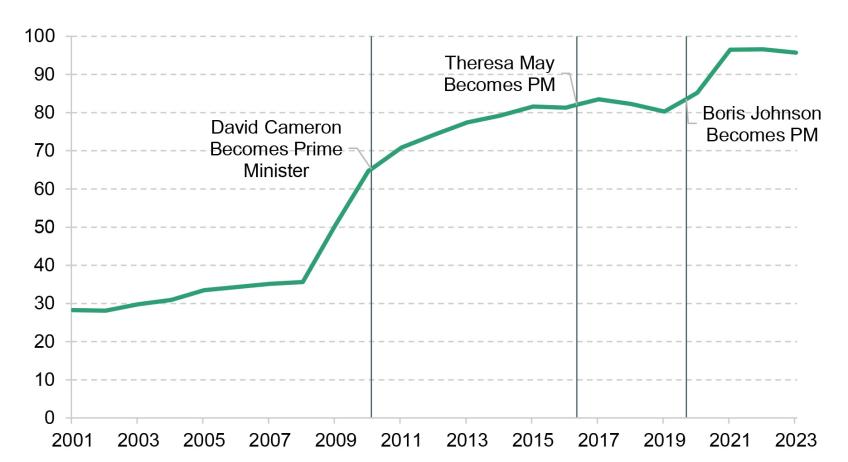

When the Conservatives came to office in 2010, they pledged that their first priority was to ‘reduce the deficit and create growth’. The Great Recession resulted in very big increases in borrowing across Europe, and the UK’s total deficit amounted to 10 per cent of GDP, or £160 billion, an unprecedented level in modern times. This was seen as unsustainable both by the outgoing Labour government, and by both members of the incoming coalition government. While the coalition government planned to cut the deficit more quickly than promised by Labour, there was in truth considerable cross-party agreement on the need to focus on repairing the public finances albeit with some differences over the speed and mix of the fiscal medicine that should be administered. Debt rose from 35 per cent of GDP to 65 per cent of GDP between 2007 and 2009, and was forecast to still be increasing in 2016.

Figure 4.1 Total national debt as a percentage of GDP

Source: Office for Budget Responsibility

As Figure 4.1 shows, the road to bringing the national debt under control has been a rocky one. The deficit fell under the coalition government, though considerably less quickly than planned, in large part because economic growth was lower than expected. By 2015 debt had stabilised as a percentage of GDP. It wasn’t until the eve of the pandemic that current budget balance (borrowing only for investment) was reached, this having been the key fiscal target for most of the period. In 2015 George Osborne even legislated a supposed commitment to get to overall budget balance from the financial year 2019–20, an economically unwise move, and something rarely achieved over the last century. This target was appropriately swiftly binned in the aftermath of the Brexit referendum.

By 2019 the deficit was at normal levels of around 2 per cent of GDP and the debt stable. Since then national debt has risen again mostly as a result of the huge levels of borrowing required to cover the costs of the Covid-19 pandemic, and then big additional spending to protect households and businesses from the worst effects of the rise in energy prices13 . Even as these costs have dissipated, public spending has risen over the 2019 parliament and, despite a swiftly growing tax burden, the national debt has risen further and is now stuck rather than decisively falling.

Future governments will have to reckon with this. Getting the national debt back on a falling path will require some combination of tight spending, yet more tax increases, and a much more impressive growth performance.

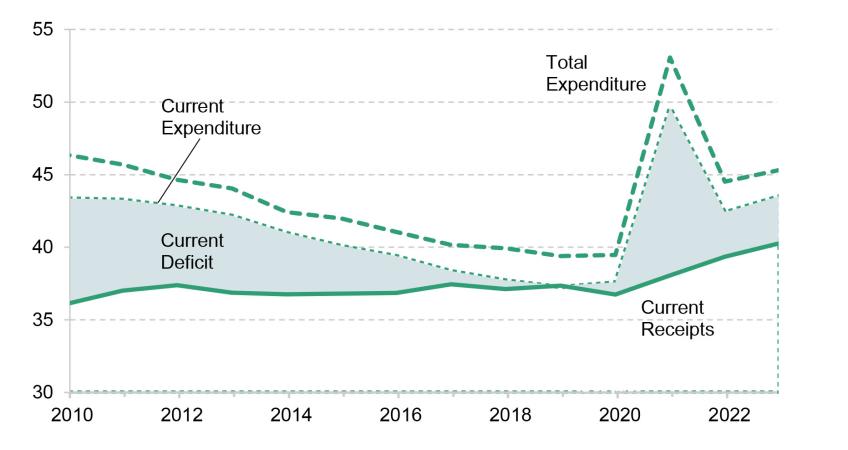

Figure 4.2 Public expenditure and receipts since 2010

Note: Each Shown as % of GDP. Current Expenditure is equal to Current Spending plus Depreciation. Total Expenditure is equal to Current Expenditure plus Net Public Investment.

Source: Office for Budget Responsibility.

Figure 4.2 plots in more detail the course of the current budget deficit since 2010. It shows how Mr Cameron and Mr Osborne leant on spending cuts, rather than tax rises, to bring down the deficit – in a ratio initially designed to be about 80 per cent spending cuts to 20 per cent tax rises, which by 2015 turned out to be more heavily towards spending cuts14 . Non-investment spending dropped from 43 to 38 per cent of GDP over the course of Mr Cameron’s premiership. This meant a real-terms cut to spending, unprecedented in modern history – more details below – though expenditure never dropped below where it was on the eve of the Global Financial Crisis. The project of eliminating the current deficit was completed under Mrs May and Mr Hammond, until the government ran a small current budget surplus in 2019. Covid and the 2022 cost of living crisis resulted in temporary surges in spending. But the 2019–24 parliament has also seen substantial permanent spending increases. This was partly a change in political direction, partly a response to the ongoing ageing of the population (with the large cohort born just after World War II now placing increasing demands on the NHS and social care systems), and partly a consequence of cuts in the previous decade being reversed to a small degree. In response, the 2019–24 parliament has seen the biggest increase in the tax-to-GDP ratio of any parliament since at least World War II, taking it to its highest level over that period.

In the rest of this section we will look at two periods separately. The first of these, 2010–19, could perhaps be split further: Mr Cameron and Mr Osborne’s time in office was focused heavily on deficit reduction and austerity. The period 2016–19 was overshadowed by uncertainties around Brexit, but fiscal policy did not change dramatically. The second period, 2019–24, saw a string of major adverse economic shocks and big increases in both spending and taxation. For each era, we will break down the key fiscal decisions that defined it.

4.1 The Coalition and Austerity (2010-2019)

The coalition government assumed office in extraordinary and difficult circumstances. The Global Financial Crisis of 2008 had led to an economic downturn and a large fiscal deficit. Net borrowing represented almost 10 per cent of GDP, a then post-war record high, as tax receipts fell and spending continued to increase. The scale of the problem was a focus of the 2010 election campaign, with the three major UK parties emphasising the reduction of the deficit as a key priority. In the run-up to the election, all three pledged to implement fiscal tightening worth almost 5 per cent of national income by 2017, though the Conservatives aimed to get there a year quicker.

Larger differences lay in the planned composition of fiscal tightening – the Conservatives’ aim was focused more heavily on spending cuts than either of the other two main parties, and this showed in their approach in government. There were some big tax increases, although also some big tax cuts, so the net tax rise was dwarfed in size by the spending cuts, which represented 5 per cent of GDP over the course of the coalition government, one of the biggest reductions as a proportion of GDP of any British government in the post-war period. More remarkably, this meant that the government cut spending in real terms, and did so on the biggest scale of the post-war era.

Of course, it was not only the UK which faced large deficits in the aftermath of the Global Financial Crisis. Much of Europe was struggling, with Spain, Greece, Ireland and others plunged into much larger fiscal crises. In terms of the scale of fiscal restraint, the UK was also not an outlier. Mostly, the level of deficit reduction a country pursued was a function of how the Great Recession affected the deficit: Ireland and Spain pursued much stronger austerity measures, Germany much weaker. Compared to other large economies with similar increases in borrowing after the crash, like France and Italy, Britain’s fiscal tightening was similar in size. Rather, what was unique about the approach taken by the Conservatives, compared even to their ideological bedfellows, was that this was mostly done through spending cuts. The centre-right governments of Italy and France at the time, on the other hand, raised taxes by more than they cut spending.15

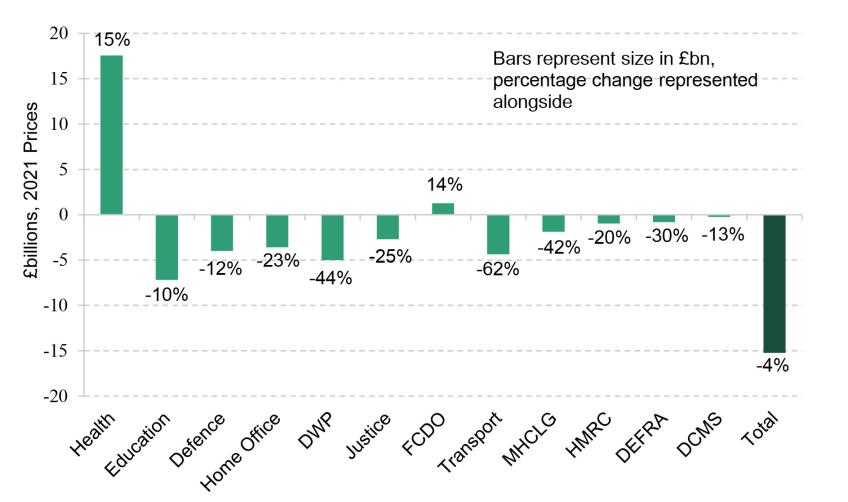

These spending cuts were felt very differently by different parts of the state. Mr Cameron and Mr Osborne specifically ring-fenced the NHS, schools and foreign aid from cuts to their day-to-day budgets. Figure 4.3 shows this variation, both in total size of change and in percentage change of non-capital spending. The Department of Health and the Foreign, Commonwealth and Development Office can be seen as the only two departments protected by budget increases. Growing pressures on the NHS meant that health resource spending actually increased by 15 per cent in real terms – though that still represented a much slower rate of growth than it had enjoyed historically, and was barely enough just to keep up with the growing size and age of the population. Despite the ring-fencing of day-to-day school budgets, other areas of education were heavily cut. The tripling of tuition fees represented a significant cut in spending for the Department for Education, though significantly increased university budgets. Further education also faced significant cuts, while flagship New Labour education policies, Sure Start and the Education Maintenance Allowance, had their funding heavily cut or were scrapped. Overall this resulted in a smaller education budget.

Areas that were not ring fenced had their budgets cut by much larger percentages. Current spending by the Ministry of Justice dropped by a quarter, with prisons, courts and legal aid all suffering cuts. Funding to local authorities from central government was cut in half over the course of the Cameron years. Those authorities most dependent on central funding – largely poorer and metropolitan areas – suffered most. Social care services, a large proportion of local budgets, were prioritised, though still faced cuts. This left other services like libraries, planning and local subsidies for public transport facing cuts often in excess of 30 per cent16 . Other central government departments, including Defence, Transport, and the Home Office also faced large cuts.

Figure 4.3 Spending changes by department, 2010-2019

Note: Size of bar represents change in £billions, figure on chart represents percentage change. X-axis ordered according to department budgets in 2010. Baseline taken as 2011 for Home Office and MHCLG, due to the transfer of police grants between them in 2010.

Source: Office for Budget Responsibility.

In the early period capital budgets were cut much more drastically than resource spending, and spread more evenly across departments. This meant, for example, significant reductions in spending on the maintenance and construction of new schools, hospitals and local government buildings. Capital spending on prisons and courts, while smaller proportions of the capital budget, also faced large cuts. These costs did not have a major effect during the period of austerity, but mean that it is likely that future governments will need increased capital spending to account for these major cuts. The health service is suffering already from poor building maintenance and lack of machinery. The problem with Reinforced Autoclaved Aerated Concrete (RAC) in schools, which came to light in 2023, cannot be put down entirely to cuts over the 2010s but will have been exacerbated by them.

The above all relates to public-service spending. Meanwhile spending on pensioner benefits was protected, and indeed increased, while working-age benefits were made less generous. The Coalition introduced the triple-lock principle for the State Pension, which guaranteed that it increased each year by the maximum of 2.5 per cent, inflation and growth in average earnings, meaning that over time it would increase relative to both prices and earnings.

Reforms to working-age benefits took a very different trajectory. Significant cuts were made to the generosity of means-tested benefits and tax credits and hence to the new Universal Credit (UC) that is still being rolled out fourteen years after it was announced17 . Delays and cuts apart, the introduction of UC, which rolled six different working-age benefits into one and which has simplified and automated the benefit system, may in the end be seen as one of the lasting achievements of the Conservative years.

Other smaller cuts proved particularly controversial, including a cut to housing benefit for working-age individuals in social housing deemed to have a spare bedroom – dubbed by its opponents as the ‘bedroom tax’. The Conservatives went into the 2015 election pledging further big – but largely unspecified – cuts to working-age welfare to be implemented within two years. Following the general election, cuts were delivered on a slower timescale, with the biggest being a four-year cash freeze to most benefits. The ‘two-child limit’, which limits means-tested support (in most cases) to only the first two children, was introduced from 2017. Its effect will grow over time as it only applies to children born after its introduction, but it has already been shown to be increasing rates of child poverty.

The taxation picture under Mr Cameron and Mr Osborne was more mixed than that of spending. Taxes rose overall. The biggest increase was an increase in the main rate of VAT from 17½ to 20 per cent, raising £13bn. Other tax increases came from National Insurance, the rate of which the government increased from 11 to 12 per cent in 2011, raising £9bn. Further increases to National Insurance came from an end to the practice of contracting out of paying some National Insurance in 2016, raising another £4bn. Substantial cuts to the generosity of caps on the amount that can be contributed to a pension each year represented a further tax increase.

At the same time, and remarkably in the context of austerity, the income tax personal allowance was increased by a third in real terms, removing 2 per cent of adults from the tax base and reducing the level of income tax for all but the highest earners, at a cost of £5bn per year. Meanwhile, the main rate of corporation tax was cut from 28 to 19 per cent between 2010 and 2018. This was partially offset by a broadening of the tax base from increased anti-avoidance measures, but the policies in combination still reduced receipts by £13bn. The additional rate of tax, paid by those on the highest incomes, was also cut from 50 to 45 per cent. The effect of this was weakened by the threshold for paying it being frozen at £150,000, and then eventually being cut to £125,000 in 2022, meaning that the number of people paying the additional rate of tax increased fourfold over the period. Finally, the real rate of fuel duties was cut consistently over the decade. Each year, planned increases to rates of fuel duties have been either delayed or cancelled, a practice that continued beyond 2019. As a result, they have been frozen by successive governments since 2011.

4.2 A New Era of Tax and Spend (2019-2024)

The 2019 election was fought on a very different manifesto to that in 2015. Rather than promising cuts the Conservatives were focused on areas demanding increased spending or investment, including plans to ‘level up’ less prosperous parts of the country, and major plans to increase investment, including large capital investment in hospitals.

The sprouts of increased overall spending could be seen earlier, however. In 2018, Mrs May pledged to return NHS spending to historical growth levels and as chancellor Mr Hammond set out a rising trajectory for capital spending. Plans for real-terms spending increases were announced by Mr Sunak in the new government’s first budget in early March 2020, just before it started to become clear how severe the Covid-19 pandemic would be.

These plans would be blown out of the water by the pandemic, as spending increased massively, and borrowing rose to 17 per cent of GDP, a level never before seen in the UK in peacetime. Most of this growth in borrowing came from £310 billion of discretionary spending to support households, businesses and public services in the pandemic. Almost half of this came in the form of direct support to households, most notably through the furlough scheme18 . The rest came from a combination of relief to firms and increased health spending, with £37bn spent on the ‘test and trace’ system and £12bn on personal protective equipment. The furlough scheme and the £20 per week uplift to Universal Credit remained in place beyond 2020, both expiring in September 2021. Meanwhile, pressures on health spending continued into the second year of the pandemic, with additional costs from high hospitalisation numbers and the vaccine rollout.

As a fraction of GDP, this increase in discretionary spending ranked towards the top of all advanced economies, with only the US spending significantly more19 .

Public spending has remained well above its pre-pandemic level, as shown in Figure 4.2, with increases quite broad based. Health spending has continued to grow as a share of the total, and demographic change will continue to push up spending on health, pensions and social care.

The second crisis of the parliament arrived with the war in Ukraine and the subsequent surge in energy costs. The government stepped in with the Energy Price Guarantee, which subsidised household energy bills, limiting the energy price cap to £2,500 per year for the average household. This was estimated to cost the government £37 billion, or 1.5 per cent of GDP20 . This enormous, and entirely untargeted, intervention was in fact announced during the short-lived Liz Truss premiership. By contrast with the £45 billion package of tax cuts, this policy remained almost completely intact, though Jeremy Hunt raised the cap to £3,000 for the winter of 2023.

Meanwhile, inflation increased to levels not seen in decades, driven in part by the energy price rises, but also by other supply constraints that emerged in the aftermath of the pandemic. The magnitude and duration of both the fiscal and monetary response to Covid also played a role. Subsequent increases in interest rates not only raised costs for mortgagors (now only 30 per cent of households, well down from a peak of 40 per cent in the mid 1990s) but also hit government finances as the cost of servicing debt grew from around 1 per cent of national income to over 4.4 per cent at its peak in 2022–3, a figure that had not been exceeded since 1948–9. While these costs will fall somewhat as inflation eases, debt interest spending is set to remain much higher than historically, and will continue to constrain fiscal policy for years to come. This is the consequence of much elevated levels of debt due to the three crises since 2008 (the Global Financial Crisis, Covid-19 pandemic and the cost of living crisis) and interest rates at higher levels than we had during the 2010s.

As the UK weathered a series of global macroeconomic shocks, the Conservatives provided a macroeconomic shock of their own. The election of Liz Truss as Conservative Party leader and prime minister led to a tumultuous forty-nine days. In a ‘mini-budget’ on 23 September 2022, her first chancellor Kwasi Kwarteng introduced a series of major tax cuts. In his time as chancellor, Rishi Sunak had promised to introduce a new health and social care levy – 1.25 per cent tax on earnings paid by employees, employers and the self-employed – supposedly hypothecated to fund increased health and social care costs, as well as the first increase in the main rate of corporation tax since 1973, from 19 to 25 per cent, each to take place in April 2023. Mr Kwarteng immediately scrapped both of these, and then added some additional tax cuts of his own, including the abolition of the 45 per cent additional rate of tax, paid by those with an income over £150,000. In total, this was estimated to represent a £45 billion tax cut, equivalent to 2 per cent of GDP, one of the largest tax-cutting budgets in history. No tax rises or spending cuts were announced to offset the cost of these cuts, and no forecast of the effects was presented, either by the chancellor – who on his arrival at the Treasury had immediately dismissed its permanent secretary – or the Office for Budget Responsibility. And the chancellor promised there would be more to come.

The markets responded swiftly and negatively. The pound fell to its lowest ever level against the dollar. Gilt rates, the interest rate on government debt, rose by over a percentage point within a week, a greater change than gilt markets normally see over the course of a year. The Bank of England intervened in bond markets to protect Defined Benefit pension schemes. Mr Kwarteng, and then Ms Truss, were ejected from Downing Street. Their replacements, first Jeremy Hunt as chancellor and then Rishi Sunak as prime minister, swiftly reversed most of the tax cuts, though the health and social care levy was not reintroduced. Gilt rates dropped back down to near their level before the mini-budget upon their replacement, before increasing broadly in line with interest rate rises by the Bank of England.

The biggest tax rise of the 2019 to 2024 parliament, though, came about through the freezing of income tax and National Insurance thresholds, initially for four years (announced by Mr Sunak as chancellor in 2021) and extended to six by Mr Hunt. In an era of high inflation this now looks set to be a £40 billion a year tax rise. It will undo two-thirds of the increase in the income tax personal allowance which was such a centrepiece of the coalition’s tax policy between 2010 and 2015, and will result in a near doubling of the number of higher-rate taxpayers. In a final twist in November 2023, Mr Hunt announced a cut in National Insurance from 12 to 10 per cent, more than reversing the increase put in place by Mr Osborne in 2011. Despite costing £10bn, this tax cut is far smaller than the amount raised by freezing personal tax thresholds through fiscal drag.

The overall effect of these policies will be to take tax as a fraction of national income to its highest ever level. The 2019–24 parliament will see taxes rising by more than any other parliament since at least 1950. Elevated debt – and with it debt interest spending – slow growth and pressure to spend more on health, pensions, defence and many other areas of public provision, suggest to us that this high level of tax is here to stay.

5. Monetary Policy

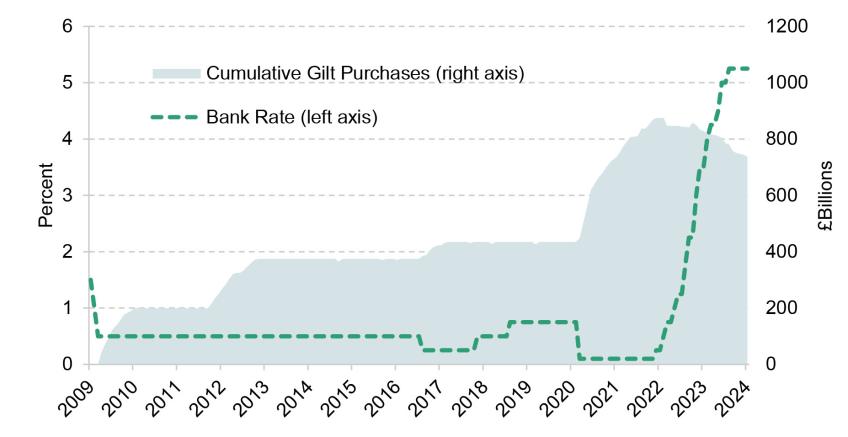

While the Bank of England has operational independence, it is impossible to understand the course of the economy over the last fourteen years without considering the role monetary policy has played. The period between 2010 and 2021 was marked by an unprecedented period of low interest rates and use of unconventional monetary policy (quantitative easing, QE). The shift to higher interest rates since 2022 has been sharp and sudden, with significant implications for both households and government debt. Figure 5.1 shows the course of monetary policy since the Global Financial Crisis, when the Bank of England began its programme of quantitative easing.

The dotted line shows that the bank rate stayed below 1 per cent from March 2009 all the way until May 2022. As the Bank’s traditional main tool for monetary policy, it was kept low in response to sluggish economic growth and fears that any tightening would risk deflation, and edged down further in response to expected negative shocks, including the Brexit vote and the pandemic. The Bank also made use of QE, in attempts to stimulate the economy. There have been a series of QE interventions following an initial injection of cash in 2009. In 2011, the Bank purchased £175 billion worth of gilts over the course of a year in an attempt to provide some additional stimulus. Another smaller programme of £60 billion immediately followed the Brexit vote. The Bank responded to the Covid-19 pandemic by reducing interest rates from 0.75 to 0.1 per cent and also by the largest QE programme of all, with over £400 billion of assets purchased over the course of less than two years, taking the total amount of money injected into the economy to over £800 billion. Given the supply constraints created by the pandemic, which are likely to have been almost as severe as the hit to demand, the scale of QE from 2020 has been described by many as excessive – former Bank of England governor Mervyn King called it ‘a terrible mistake’, and said that printing money was the last thing the Bank should have done21 .

As discussed in the section on growth, twelve years of loose monetary policy did not lead to more public investment, and business investment also remained below that of comparable countries. However, low interest rates had major distributional consequences, pushing up asset prices and benefiting those with wealth (largely older generations) at the expense of largely younger people who started the period with few assets. Younger generations have experienced much lower levels of homeownership than did older generations at the same age. Middle-income people in their early thirties are now still largely renting privately, rather like their low-income peers. Twenty-five years ago they were, like their better-off peers, largely homeowners. By contrast, homeownership rates among older generations are around 80 per cent. They benefited not only from rising asset and house prices driven in large part by loose monetary policy, but also by fiscal policy which has generally benefited those over state pension age more than the young. At the same time, as we have seen, wages have been stagnant. The combined impact of increases in asset prices and stagnant wages means it is harder for someone reliant on wages to save their way up the wealth distribution. This generational redistribution will be an important legacy of the 2010s. It also means that for younger generations inheritances are becoming increasingly important, further reducing scope for social mobility22 .

Figure 5.1 Spending changes by department, 2010-2019

Note: Size of bar represents change in £billions, figure on chart represents percentage change. X-axis ordered according to department budgets in 2010. Baseline taken as 2011 for Home Office and MHCLG, due to the transfer of police grants between them in 2010.

Source: Office for Budget Responsibility.

Assuming interest rates stabilise at levels nearer 2 or 3 per cent than the less than 1 per cent that was prevalent for so long, some of these effects may unwind a little as asset prices partly fall back – though the immediate pain will be felt by a relatively small group of the population: those largely in their thirties with big outstanding mortgages relative to their earnings. By 2023 we had already seen a fall in household wealth fall by around one-third of national income.

As we saw above, the combination of higher interest rates and weak growth is also having a major effect on the public finances. It means that for the next few years at least we will need to run primary surpluses – that is raise more in revenue than we spend on everything other than servicing the national debt – just to stop the national debt being on an ever-increasing trajectory. That is not something that has been achieved since 2001–2.

6. Conclusion

The period between 2010 and 2024 has been extraordinary from an economic point of view. For most of the period, interest rates were at their lowest level in history. Earnings grew at probably their slowest rate in more than 200 years. The period from 2010 to 2019 saw the biggest and most sustained cuts in public spending since World War II. These changes accelerated a trend which saw older generations and those with substantial assets doing far better than younger generations.

Brexit led to a complete reappraisal of our trading links with the European Union, and created huge economic uncertainty. The response to the Covid pandemic involved unprecedented levels of public support for the economy, and borrowing on a scale even greater than that seen during the financial crisis which set the context for the period as a whole. Taxes rose by more during the 2019–24 parliament than in any parliament since at least 1945.

The period of low interest rates came to an abrupt end from 2022 when a combination of international and domestic pressures forced up inflation. Real earnings and real incomes fell. The legacy for the next government will be a difficult one. Expected economic growth is slow. The fiscal policy responses to the three shocks of the financial crisis, Covid-19 and the cost of living crisis mean that public sector debt is high, and a combination of high interest rates and low growth means that even running a primary surplus will not be enough to get it on a downward trajectory. That primary surplus appears to be achievable only with a combination of further tax rises – from a record high base – and extremely tight spending settlements. As of autumn 2023 spending plans for the period after the election imply cuts for many departments, which we might suspect will not be delivered.

High debt, low growth, and high interest payments have arrived at a particularly difficult time. Demographic pressures are starting to tell. It is hard to see how health spending – the biggest part of public spending – will do anything other than rise quite swiftly over the coming years. The share of adults over the state pension age will also increase, and pressures on social care are intense. International pressures and commitments mean that defence spending, a traditional source of savings to spend elsewhere, is more likely to have to rise than be available for cuts. Most other areas of public spending suffered cuts through the 2010s which look hard to repeat.

Through all this the Coalition and Conservative governments made some big choices. The first was to focus on deficit reduction achieved largely through spending cuts in the first half of the 2010s. This included big cuts in investment spending, which are likely to have created longer-term problems not only for economic growth but for the performance of public services. Many other countries chose a more even balance between tax rises and spending cuts. Like previous governments they, relatively, prioritised health spending over spending on other public services. They chose to increase the level of state pensions while cutting working-age benefits – thereby exacerbating the distributional consequence of loose monetary policy. The introduction of Universal Credit is likely to be seen as a lasting, if vastly delayed, achievement. Overseas aid spending rose swiftly to 0.7 per cent of national income, though has since been pared back to 0.5 per cent. Local government, the justice system, prisons, have faced among the biggest spending cuts, and have struggled to cope.

In most respects tax policy has been notable only for its inconsistency. Quite contrary to initial intentions the legacy will be an income tax system in which far more people are paying higher rates of tax, and with more taxpayers than ever. The corporation tax, initially cut sharply, will be raising more as a fraction of national income than it has before in the UK on a sustainable basis, and more than in most OECD countries. VAT was raised straightaway and remains at 20 per cent, but it also remains unreformed and applicable to, by international standards, an unusually small fraction of spending. The one consistent change is the one that was denied in every Budget – each and every year chancellors promised that rates of fuel duties would rise in line with inflation in the following year, and each and every year they failed to do so. A much lower real rate of fuel duties and no plan to move to any form of taxation for driving electric vehicles is another unwanted legacy which the next government will need to deal with.

The growth and productivity slowdown from which the British economy suffered was far from unique among developed country economies. But on most forecasts the future looks harder. Inflation is higher in 2023 than in either the US or the Eurozone. Private investment and trade intensity fell relative to our competitors after the Brexit vote and implementation. Productivity per hour worked is 13 per cent less than in Germany and 8 per cent less than in France. On purchasing power parity metrics median household income is 22 per cent below Germany.

There are opportunities. A return to stable government with reasonably consistent economic policy should be enough to make some progress. There are evident opportunities to improve growth through shifting policy on investment, education, planning, tax, trade and elsewhere. But an incoming government will need to pursue any such policies from the starting point of a most precarious fiscal situation. In a now infamous note the last chief secretary to the Treasury in the last Labour government told his successor ‘there is no money’. That remains true today.

Endnotes

Authors

Carl Emmerson

Carl, a Deputy Director, is an editor of the IFS Green Budget, is expert on the UK pension system and sits on the Social Security Advisory Committee.

Paul Johnson

Paul has been the Director of the IFS since 2011. He is also currently visiting professor in the Department of Economics at University College London.

Nick Ridpath

Nick joined the IFS in 2023 and works in the Education and Skills sector, focusing on the long-run impacts of education policy.

More from IFS

Understand this issue

Policy analysis

Academic research