Today the Office for National Statistics and HM Treasury published Public Sector Finances January 2017. We now have details of central government receipts, central government spending, public sector net investment, borrowing and debt for the first ten months of financial year 2016−17.

Thomas Pope, a Research Economist at the IFS, said:

“It is usual for large surpluses to be run in January, but even so this month’s numbers contained particularly good public finance news. This was the largest monthly surplus since 2000, as strong growth in receipts boosted the government coffers. A simple extrapolation implies that government borrowing could be up to £12 billion lower this financial year than the OBR forecast in November – at around £56 billion. Accounting changes means this overstates the good news slightly – but even on a like-for-like basis borrowing is likely to end up between £5 billion and £10 billion lower than the OBR forecast.

While self-assessment income tax receipts disappointed a little relative to forecast, it was a strong month for receipts overall with PAYE income tax, capital gains tax, VAT, Stamp Duties and corporation tax all on course to raise more than the OBR forecast for this financial year back in November. With just two months of the year to go, and after adjusting for an accounting change to corporation tax which boosts measured receipts by £3 billion, central government receipts could be up to £5 billion higher than forecast in November.

The news on the spending side is also positive, and Central Government is currently on course to undershoot forecast spending for the year as a whole. Part of this undershoot is likely to reflect differences in the timing of local authority grants and EU transfers, and so does not imply any improvement in the underlying public finances. The timing of other elements of public spending can also vary so we will have to wait and see whether spending by central government departments rebounds in the final two months of the financial year or whether a significant underspend is delivered.”

Further analysis

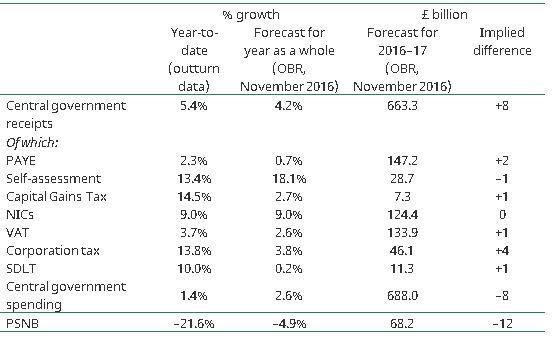

Receipts

Extrapolating from the first ten months of this financial year, Central government receipts are set to be £8 billion higher than the OBR forecast in November (see Table), though still lower than the March 2016 forecast. This is due to PAYE income tax, capital gains tax, VAT, Stamp Duties and corporation tax all exceeding expectations.

The reason for the large overall surplus that was run in January was self-assessment receipts, which are mostly scored in that month. However, income tax self-assessment actually disappointed relative to forecast. It is important to note that self-assessment receipts were particularly uncertain this year as a change to the taxation of dividends meant that some owners of small companies had the incentive to forestall dividend payments, taking more in 2015–16 (the receipts for which came in this January). Therefore, the disappointment on self-assessment receipts may simply reflect less forestalling rather than bad longer term news for the public finances.

Corporation tax is now counted on an accruals basis, rather than a cash basis. This increases revenues this year by around £3 billion. Even so, this was a good month for corporation tax revenues, and on a like-for-like basis corporation tax receipts are on course to exceed the OBR forecast by over £4 billion.

Table: Growth in receipts, spending and borrowing over the year to date

Note: PAYE = Pay As You Earn; NICs = National Insurance Contributions; SDLT = Stamp Duty Land Tax; PSNB = Public Sector Net Borrowing Total growth figures refer to Central government only. Corporation tax is presented on a cash basis, rather than an accruals basis. Numbers may not sum due to rounding.

Spending

The figures for this year so far imply that spending by Central Government may undershoot the OBR forecast by up to £8 billion. Debt interest spending and welfare spending are both broadly on course to meet their forecast, with the current forecast underspend coming from current spending of government departments. Part of this difference reflects the timing of EU transfers and grants to Local Authorities. It may be that underspends will still be achieved, but it could also be the case that spending catches up with the forecast over the final two months of the year, such that spending comes in closer to what the OBR expects.

Further information and contacts

For further information on today’s public finance release please contact: Carl Emmerson or Thomas Pope on 020 7291 4800, or email [email protected] or [email protected].

Next month’s public finances release is due to be published on Tuesday 21st March 2017.

Relevant links:

This, and previous editions of this press release, can be downloaded from http://www.ifs.org.uk/publications/browse?type=pf

Office for National Statistics & HM Treasury, Public Sector Finances, January 2017: http://www.ons.gov.uk/economy/governmentpublicsectorandtaxes/publicsectorfinance/bulletins/publicsectorfinances/jan2017

Office for Budget Responsibility analysis of monthly Public Sector Finances, January 2017: http://budgetresponsibility.org.uk/monthly-public-finances-briefing/

Office for Budget Responsibility, Economic and Fiscal Outlook, November 2016: http://budgetresponsibility.org.uk/efo/economic-and-fiscal-outlook-november-2016/

HM Treasury Autumn Statement 2016: https://www.gov.uk/government/topical-events/autumn-statement-2016

Ends

Notes to editors

- Central government current spending includes depreciation.

- Where possible we compare figures on an accruals basis with the Office for Budget Responsibility forecasts.

Authors

Carl Emmerson

Carl, a Deputy Director, is an editor of the IFS Green Budget, is expert on the UK pension system and sits on the Social Security Advisory Committee.

Thomas Pope

More from IFS

Understand this issue

Policy analysis

Academic research