Yesterday was a big day for local government in England. The Department for Communities and Local Government (DCLG) published the ‘Provisional Local Government Funding Settlement’ – which sets out how much in the way of core grants it plans to give each English council every year between 2016–17 and 2019–20. The settlement will result in cuts in local councils’ spending power of around 8% on average – a much smaller scale of cuts than experienced over the last parliament. The cuts will also be more evenly spread, rather than hitting poorer authorities harder as happened between 2010 and 2015. With the additional ability to increase council tax to pay for social care, the average council tax bill for a band D property could rise by £205 a year by April 2019 if these powers are used in full, with the potential for further rises to pay for police and fire authorities.

As in the last parliament, grants to councils are set to be cut substantially over the next 4 years. Taken together, the amount councils receive in Revenue Support Grant (RSG) and other grants from DCLG are set to fall by 60%.

But councils also have other sources of revenue: they retain a portion of business rates revenues and levy and retain council tax, and taken together these are a much bigger source of revenue than grants from DCLG. And these revenue sources are expected to grow over the next four years, not least because councils are expected to raise council tax fairly significantly.

Looking at how much councils will have to spend in total, including these additional sources of revenue, the cuts will be around 7% in real terms over the next four years. This is a substantially slower pace of cuts than councils had to deliver between 2009–10 and 2015–16, when councils’ spending power was cut on average by 25% in real terms. Cuts over the next four years, though, will be front loaded, with cuts of around 4% to 5% next year, on average.

These figures are national averages though, so how might the cuts affect different councils?

The impact of cuts across councils

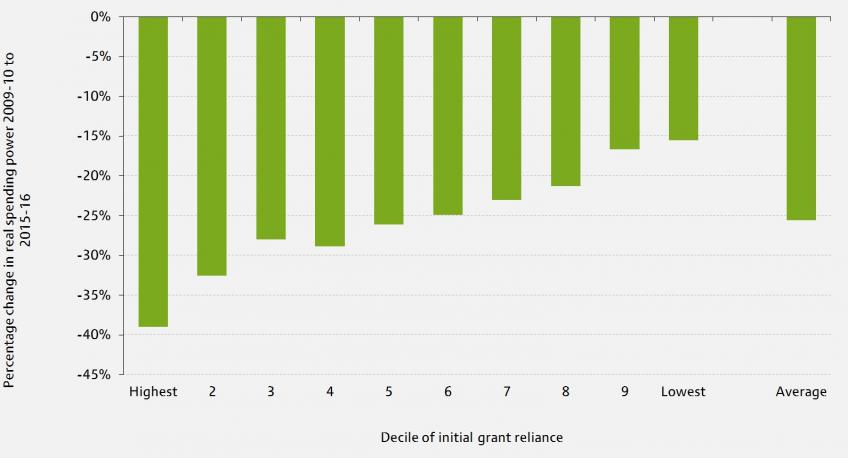

Figure 1 shows that over the course of the last parliament, cuts in spending power were much greater for those councils which rely a lot on grants for their funding – because they have low council tax bases, or high spending needs for instance (i.e. they are poorer) – than those less dependent on grant. In the last few years, DCLG effectively cut every council’s grant by the same percentage. Of course, a given percentage cut in grant has a bigger impact on a council if it relies more on that grant for its overall spending.

Figure 1. Percentage change in real spending power 2009–10 to 2015–16 by initial grant reliance of local authority

Source: DCLG, Local authority outturns and budgets.

Note: Greater London Authority non-police, non-fire spending power allocated to London councils in proportion to population.

But this pattern is set to change because of a change in the way DCLG allocates cuts to grants across councils. It now explicitly takes into account the differing extent to which councils rely on grants, making smaller cuts to the grants of those which rely a lot on the grant than to those councils which are able to raise more of their own revenue from council tax.

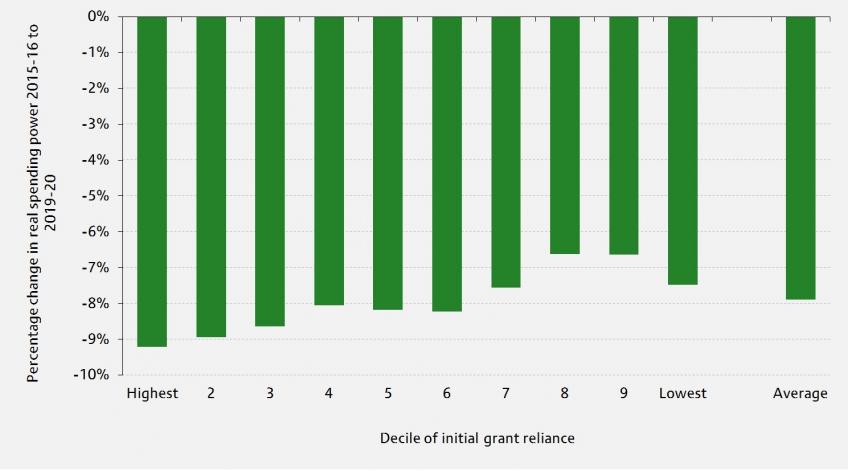

This means, looking ahead over the next 4 years, cuts to spending power will be much more evenly distributed across councils than they were over the last parliament – as shown in Figure 2. Nevertheless, cuts will still be a bit larger on average for (principally poorer) areas who are most reliant on grant (for which cuts are set to average 9.2%), than for those who are least reliant on grant (for which cuts are set to average 6.8%).

Figure 2. Percentage change in real spending power 2015–16 to 2019–20 by initial grant reliance of local authority

Source: DCLG, Core spending power: provisional local government finance settlement 2016 to 2017.

Note: Greater London Authority non-police, non-fire spending power allocated to London councils in proportion to population.

Why is a bigger squeeze on poorer councils still happening if DCLG is now accounting for differences in reliance on grant funding? It is because, while DCLG’s new allocation of funding accounts for the initial level of grant reliance, it does not account for the fact that things change over time as councils’ other sources of revenue – notably council tax – grow. In particular, the forecast growth in council tax rates and revenues will do less to offset cuts to grants in areas with small council tax revenues and a high degree of grant reliance than it does in areas with large council tax revenues and a low degree of grant reliance. In other words, it is the fact that the poorer, more grant-dependent areas can do less to increase their budgets by increasing their council tax that means they will still fair a little worse over the next few years than leafier, less grant-dependent places.

Spending cuts will differ not only across different local authorities but also across different areas of spending, just as it did over the last five years (an IFS briefing note published before this year’s general election provides analyses in detail the cuts to local government spending between 2009–10 and 2014–15). Looking to the next four years, spending on adult social care is likely to be particularly protected, because some of the grant to authorities is being ring-fenced for this purpose and because councils are being given the ability to raise council tax by an additional 2% a year specifically to fund adult social care. If this ring-fenced funding and council tax revenue were used to stop further cuts to adult social care and instead offer a real-terms freeze – which may not be enough given rising demands and cost pressures – real-terms cuts to other areas of spending would need to be around 12%, on average, by 2019–20. This could mean difficult choices for other services like children’s social services, refuse collection, libraries, transport, economic development, planning and housing, some of which have already seen very large cuts. Every additional 1% increase in adult social care spending would require additional cuts to other areas of spending of around 0.5%.

Council tax

The extra council tax ‘precept’ for social care not only affects councils’ budgets, it will also affect how much council tax households pay.

Over the last few years, councils wanting to raise council tax by more than 2% have had to call a referendum. None have done so (although Bedfordshire police tried and failed to win such a referendum on the local police precept). Councils with social care responsibilities will now be able to increase council tax by a further 2% – i.e. a total of 4% – without a referendum. Other councils like districts and the Greater London Authority will still only be able to raise rates by 2% a year without a referendum.

If councils make full use of these powers, the average Band D rate in England would go up by £48 a year next April (£33 in real terms), and £205 a year by April 2019 (£97 in real terms). However, it is important to note this will follow a 5-year period when most councils have been freezing their council tax, leaving the average council tax bill a little lower in real-terms in 2019 than in 2010.

Of course, councils may not make full use of the powers. DCLG assume that councils will make full use of their social care precepts but only increase council tax rates otherwise by 1.75%, rather than the full 2% ‘standard’ rise they are allowed without a referendum. This would see council tax increasing by £191 a year by April 2019 (£84 in real terms). However, if further cuts to services become too difficult to bear, some councils might hold referendums for bigger council tax rises. And police authorities and fire authorities also levy council tax precepts – increases in either of these would push council tax bills up further.

The local government financial revolution

Taken together yesterday’s local government financial settlement therefore has some big changes in it: an easing in the pace of cuts, a change in the way cuts are allocated across councils, and the return of rising council tax bills.

Bigger changes are on the horizon though. The government will soon begin consulting on how to fully devolve business rates revenues to councils. This change, planned to take place by 2020, will mean councils’ spending power in future will be more directly linked to the performance of the local economy, – meaning additional incentives to encourage growth, but greater risk when things go wrong. A key thing still to be decided is just how much divergence between the revenues of different areas should be allowed before safety net systems kick in.

The full localisation of business rates will also represent a significant transfer of additional money to councils and the government will be asking councils to take on additional responsibilities in return for this extra money. Just what these extra responsibilities will be is as yet undecided – but it may include things like police, or public health, or even the operation and funding of parts of the benefits system (e.g. attendance allowance, which is a benefit paid to disabled pensioners).

Yesterday’s announcements are, therefore, just part of some genuinely revolutionary changes that are taking place to local government finance.

Authors

David Phillips

David is Head of Devolved and Local Government Finance. He also works on tax in developing countries as part of our TaxDev centre.

David Innes

More from IFS

Understand this issue

Policy analysis

Academic research