On Wednesday 6 March the state pension age for men and women reaches 65 and 3 months. This is the first time since the 1930s that men and women could only first receive the state pension at an older age than 65. As well as reducing government spending the increases in the female state pension age since 2010 have led to some – but not most – remaining in paid work for longer. This observation provides more detail on what the impact of the rising state pension age is likely to be on retirement behaviour.

From 1940 until late 2018 the male state pension age (SPA) was 65. Over this period, male life expectancy has risen substantially. Male life expectancy at birth rose from 71 in 1980 to 79 today, while male life expectancy at age 65 rose from 13 years in 1980 to 18½ years today.

Since December last year the state pension age for men is no longer 65. A man born on 6th December 1953 – who turned 65 on 6th December 2018 – was not able to claim a state pension then, but can first do so from tomorrow (Wednesday 6th March), at the age of 65 and 3 months. For those entitled to a full single-tier pension, which is currently worth £164.35 a week, a three-month delay means a total loss of just over £2,100 of state pension income.

It is not only men whose state pension age is rising above 65, it is happening for women too. Following almost nine years of gradual increases in the SPA for women from 60 to 65, for the first time since 1940, both men and women now have the same state pension age. By September 2020, the state pension age will have risen to age 66 for both men and women.

The increase in the female state pension age from 60 to 65 was legislated in 1995. The intention to increase the state pension age beyond 65 was first legislated in 2007. In 2011, the Coalition government brought forward the increase in the state pension age for men and women from 65 to 66 from Spring 2022 to the end of 2018. The 2011 Pensions Act also accelerated the increase in the state pension age from 63 to 65 for women between 2016 and 2018.

These increases in the state pension age have been controversial. But they save the government a lot of money. Previous IFS research found that the increase in the female state pension age from 60 to 61 saved the government around £2 billion per year. Further increases will have been likely to deliver savings of a similar magnitude. The Department for Work and Pensions estimates that, were they to have to compensate women for the rise in the pension age covering the period up to 2020–21 it would cost £77 billion, with greater annual spending thereafter.

The potential impact on retirement behaviour

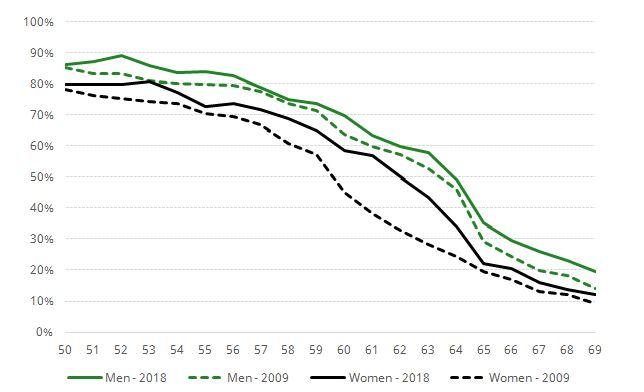

Predicting the impact on retirement behaviour of increasing the state pension age for men and women to 66 is difficult. We can look at the increase in the SPA for women from 2010 to 2018 as a potential guide. Figure 2 shows the proportion of men and women who were in paid work, between the ages of 50 and 69 in 2009 (when the SPA for women was last 60) and 2018 (when it was reaching 65). There was no change in men’s state pension age in this period.

The first thing to note from the figure is that not all men and women retire at the state pension age: employment rates fall from age 50, with fall accelerating once people reach their late 50s..

For men, there were slight increases in the employment rate between 2009 and 2018 across most ages 50 to 69. The increases in the proportion of women in paid work between the ages of 60 and 64, though, are particularly striking. For example, the employment rate of 60 year olds has risen from 45% to 58% since 2009. Up to 10 percentage points of this increase 13 percentage point increase can be directly attributed to the increase in the state pension age (see Cribb and Emmerson 2018). These increases have brought the employment rates of older women closer to those of older men, with further convergence likely to occur in future years (see Banks, Emmerson and Tetlow 2018).

Figure 1 Proportion of men and women in paid work, by age, 2009 and 2018.

Source: Authors’ calculations using the Labour Force Survey. Notes: 2018 only includes Q1 to Q3. Employment includes employees and the self-employed.

The effect of the rising female state pension age on employment rates of women aged over 60, but below their (now higher) state pension age, has been large. However the vast majority of women did not delay retirement as a result of a higher state pension age. Between 35% and 40% of women have already left paid work by age 60 and do not return to paid work just because their state pension age is now higher. In addition, around half of women retire after 60, but have not delayed their retirement in response to the higher pension age.

So what can we say about the potential effect of the rise in the SPA for men and women to 66? We might expect reasonably large increases in employment – in particular among men aged 65.

In 2018 the employment rates of men moving from age 64 to 65 dropped by 14 percentage points (from 49% to 35%) while the employment rates of women dropped by 12 percentage points (from 34% to 22%). Those who do respond by delaying their retirement might end up with incomes higher than they would otherwise have been: average (median) weekly earnings of men aged 64 who were employees in 2018 was £425 while for women the equivalent figure was £288. Those who do not retire later will see their incomes reduced – with this loss depending on the extent to which higher income from working-age benefits (for example from Universal Credit) compensates for the delayed receipt of the state pension. Those who are not in paid work and not receiving other benefits will need to rely on other sources of income, such as the earnings of their spouse or their private pension pots, to tide them over until they do receive the state pension.

Authors

Carl Emmerson

Carl, a Deputy Director, is an editor of the IFS Green Budget, is expert on the UK pension system and sits on the Social Security Advisory Committee.

Jonathan Cribb

Jonathan is an Associate Director and Head of Retirement, Savings and Ageing sector, focusing on pensions, savings and later-life economic activity.

More from IFS

Understand this issue

Policy analysis

Academic research