The Department for Work and Pensions today published the recommendations of the Government’s review into automatic enrolment. This focussed on issues around membership of, contributions to, and engagement with, workplace pensions. Over the last year I served on an expert advisory group to the review. In this piece I look at two of the recommendations – both of which are likely to boost the amounts going into workplace pensions – and the proposed trials of ways to boost pension saving among the self-employed who are not covered by automatic enrolment.

Automatic enrolment before the review

Prior to today’s review automatic enrolment worked (roughly) as follows. Employers had to enrol employees aged between 22 and their State Pension Age (SPA) who earned over £10,000 into a workplace pension. Contributions to the pension had to be a minimum of 2% of earnings between the Lower Earnings Limit (LEL, £5,876 in 2017–18) and an upper limit (£45,000), with at least 1% of this coming from the employer. These minimum contribution rates are to rise to 5% (with at least 2% coming from the employer) in April 2018 and to 8% (with at least 3% coming from the employer) in April 2019. Once enrolled employees can then choose to leave the scheme if they want. If they leave, they would not have to make any employee contribution, but they would also lose the employer contribution.

Employees who earn above the LEL but who are not automatically enrolled because they are aged 16 to 22, aged over the SPA (but under age 75), or because they earn under £10,000 can actively choose to join a workplace pension. If they do they will also benefit from an employer contribution of at least 3% of earnings above the LEL. Those earning below the LEL can also choose to join a workplace pension if they wish, but their employer is not obliged to make any contribution.

Previous IFS research, published last year, has shown that so far automatic enrolment has boosted workplace pension membership substantially, with particularly large increases in membership among lower earners and younger individuals.

Proposed reforms to automatic enrolment

The Government is proposing important changes to these parameters. First, minimum contributions will be based on all earnings up to £45,000 rather than starting at the LEL. Second, the lower age limit is to be reduced from 22 to 18. The plan is for both of these changes are to happen in the mid 2020s. This timetable is to ensure that the increase in employer obligations occur after the current period where default minimum employer contributions are rising (from 1% to 3% of band earnings) and the National Living Wage is being increased faster than average earnings.

Removing the lower earnings threshold would mean that the default minimum contributions of those earning above the LEL who are in a workplace pension rises from 8% of earnings above the LEL to 8% of all earnings (up to £45,000). In addition those earning below the LEL (who are aged between 16 and 74) would, if they choose to join a workplace pension, receive an employer contribution.

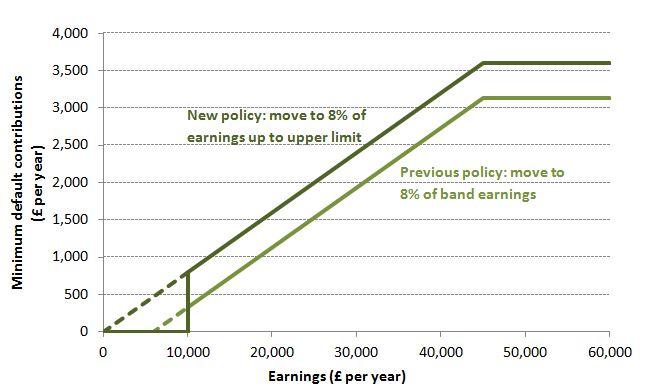

The impact of this change on default minimum contributions is shown in the Figure below. The solid lines show the total default minimum contributions (from employee and employer) before and after today’s proposal for those who earn over £10,000 and are therefore automatically enrolled. The dotted line shows the minimum contributions for those who earn below £10,000 (and therefore might not be automatically enrolled) but who actively choose to join a workplace pension.

Figure. Minimum total contributions to workplace pensions, before and after today’s proposals

For all employees earning above the LEL and only making minimum contributions the increase is worth £470 per year, of which at least £176 per year would be in employer contributions. While a relatively small amount it represents a large increase in the default minimum contribution of lower earners. For example an individual earning £10,000 would see their default minimum contribution more than double from £330 per year to £800 per year (from 3.3% of their earnings to 8.0% of their earnings). In addition the removal of the LEL would be of particular benefit to employees with multiple jobs, since they will now be able to receive employer contributions worth at least 3% of their total earnings, whereas under policy prior to today their employers might each have contributed 3% of their earnings in excess of the LEL in each of their jobs. In addition to increasing pension contributions this reform would also be a welcome simplification and reduce the risk that some employees mistakenly think that they are contributing 8% of their earnings to a workplace pension when in fact they are only contributing 8% of earnings above the LEL. (Of course those earning above £45,000 will have contributions of 8% up to £45,000 rather than 8% of all earnings.)

The reduction in the minimum age from 22 to 18 would also be likely to boost pension contributions. While those aged under 22 have seen a sizeable increase in membership of workplace pensions as a result of automatic enrolment they are still less likely to be a member of a plan than older individuals. This also feels a welcome move: in fact there is a case that the Government should have gone further and removed the age limits altogether, which would have led to all employees aged 16 to 74 earning above £10,000 a year being automatically enrolled into a workplace pension by their employer.

Taking the removal of the lower-earnings threshold and the lowering of the lower age limit from 22 to 18, the DWP estimates that this would boost contributions to workplace pensions by £3.8 billion, with £1.8 billion coming from employees, £1.4 billion from employers and £0.6 billion from up-front tax-relief. This compares to the DWP’s estimate of an additional £19.7 billion being contributed to workplace pensions as a result of automatic enrolment under existing policy in 2020. Who actually bares the cost of these contributions would be much more difficult to know: for example employers might seek to cover the cost of their contributions by slowing wage growth over coming years (as the Office for Budget Responsibility assumes in its forecasts) or by pushing up their prices.

Automatic enrolment for the self employed?

Finally the self-employed are not covered by automatic enrolment. The review does not propose a straight extension of the policy to them. This is sensible. The self-employed do not, by definition, have an employer and therefore forcing them to enrol themselves in a pension that they can subsequently choose to leave would seem odd.

Instead the Government is proposing that, in the light of the emerging lessons from automatic enrolment for employees, alternative reforms that use similar mechanisms are trialled. One leading contender would be through the tax return process. When the self-employed file their tax return they could be informed about the amount of pension saving an employee with a similar amount of income would, by default, do. This – perhaps alongside a simple process for making a pension contribution at this point – could help nudge them into a greater level of retirement saving. But we do not know how effective this would be and therefore a test and learn approach is appropriate.

One for the future

One key question remains unanswered: when minimum default contribution rates have risen to 8% of earnings should they stay there or should they be increased even further? The Government has appropriately held off making recommendations on this until evidence is available on what happens when the contribution rates rise from their current low levels. But unless the increase in minimum contributions, from 2% to 8%, that are scheduled occur over the next two years lead to a significant increase in the numbers of employees choosing to opt out of their workplace pension there will be a strong case for further increases. By the mid-2020s the nudge could be even bigger.

Carl Emmerson, Deputy Director Institute for Fiscal Studies, and member of the expert advisory group to the DWP’s review of automatic enrolment.

Authors

Carl Emmerson

Carl, a Deputy Director, is an editor of the IFS Green Budget, is expert on the UK pension system and sits on the Social Security Advisory Committee.

More from IFS

Understand this issue

Policy analysis

Academic research